Donors and nonprofits must obtain an accurate intellectual property valuation for non-cash gifts or else face potentially long or costly interactions with tax authorities.

By Kemp Moyer, Director, Advisory

Despite a historic recession and pandemic, Americans last year donated a record $471 billion to charities and nonprofits. The donated resources went to causes across the spectrum, from feeding the poor to researching treatments or cures for deadly diseases like cancer and AIDS. There was also a surge in contributions to social justice causes and support for communities through the fallout from Covid-19. For nonprofits and charities, consistent donations are essential for survival, as many of these organizations work on slim budgets or compete for a limited number of federal or state grants. And yet without these crucial services, the lives of millions of Americans — and even more globally — would be negatively affected.

For donors, gifting has many benefits. The most important is the knowledge that they are helping to make the world a better place. Additionally, there are often tax benefits to making a charitable donation. Cash donations are relatively easy to understand and record for both the donor and the recipient. However, it becomes more challenging when the donation's value isn’t as easily defined, as is often the case with privately held stock certificates, thinly traded cryptocurrencies, or the even-more-intangible category of intellectual property. Nevertheless, accurately appraising these donations is crucial for both the charity and the donor.

Intellectual Property Valuation Challenges

Donating items of value other than cash raises a unique challenge for both the donor and the charity, be it stocks, bonds or even property. The IRS requires the item's fair market value at the time of the donation to be accurately appraised at the time of the donation and reported by the donor with adequate disclosure in their tax filings. This process can be reasonably straightforward for publicly-traded securities like listed stocks or bonds, especially if the shares are relatively liquid. The charity can more simply records the stock's closing price for that day (assuming there are no restrictions). A car valuation may also be relatively simple. Homes, buildings and land can become more of a process for an adequate appraisal, as no two pieces of real property are the same – accordingly, a qualified appraisal will be an important requirement for such donations.

Beyond the above, there are many cases where determining an accurate and supportable valuation is much more challenging, and intellectual property is one of them. That’s why it’s imperative for both the donor and the charity or nonprofit to have a qualified appraiser provide a fair market valuation to these gifts as early as possible.

What Counts as an Intellectual Property Donation?

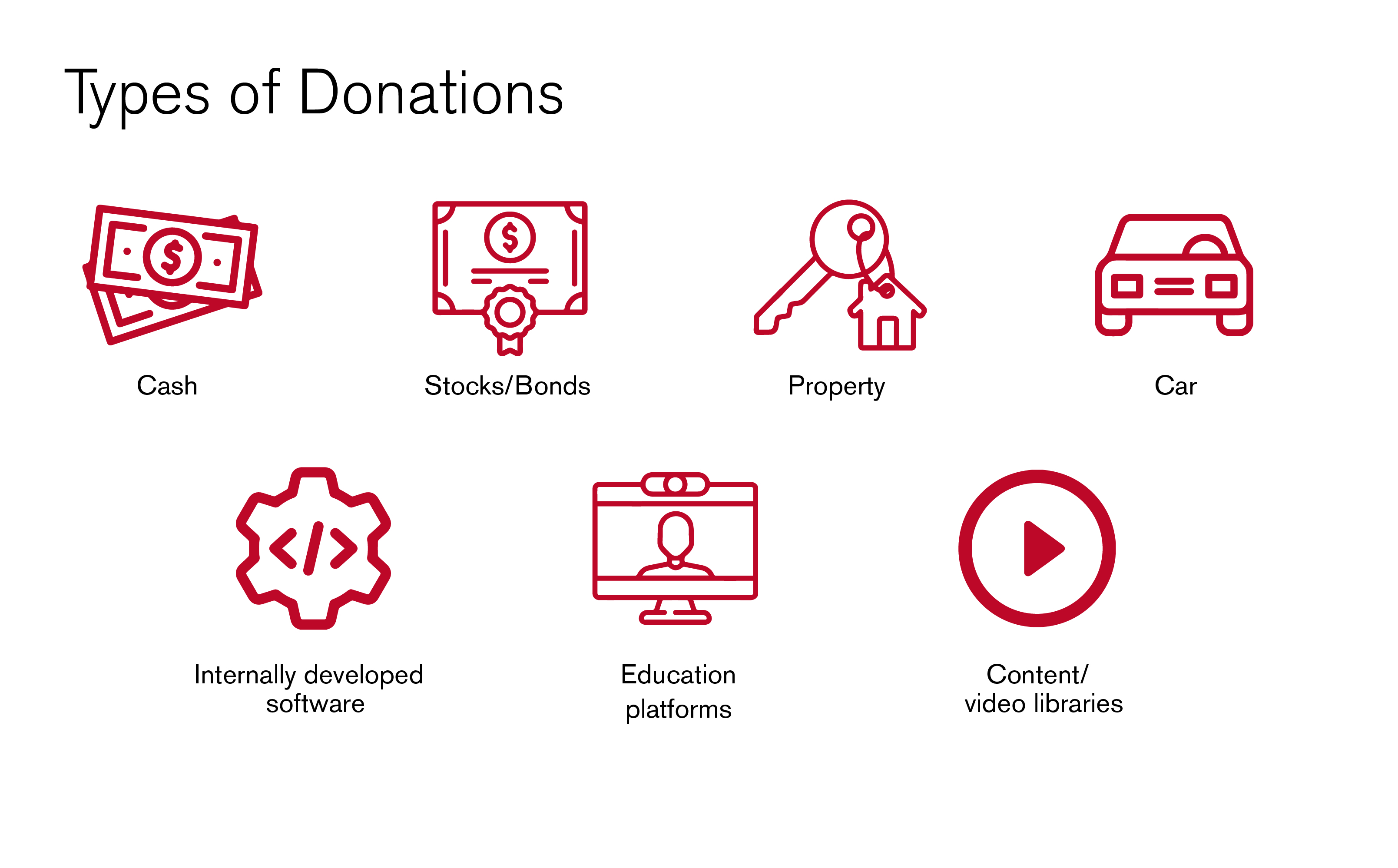

Donors may gift different types of intellectual properties to a nonprofit or charity. Examples include:

- Internally developed software

- Education platforms

- Content/video libraries

- Patents

For donations of IP, there are three techniques an appraiser can select from to determine the estimated fair market value. The first is the cost-based approach, which looks at how much it would cost to develop a similar replacement intellectual property. This includes calculating key factors like time, money and qualifications of effort expended.

An income-based approach is another method used by appraisers. Under this model, the appraiser considers how much a market participant would need to spend to license the software. Key inputs include the development of supportable estimated revenue streams and comparable royalty agreement rates.

Finally, an appraiser can use a market-based approach, which is similar to estimating the value of a house: An appraiser looks for similar transactions to get a comparative valuation.

A Note on Restricted Stock Valuations

Donors occasionally put restrictions on their gifts, such as a donation of stock that the nonprofit cannot sell for a set period of time. The donor might have several reasons for doing so. For example, if the shares were sold immediately, it could harm their other investments. Or the shares are literally restricted stock and fall under Securities Act Rule 144. Because of these restrictions, the shares are now illiquid, and there may be discounting applicable to their fair market value. This is another situation where a qualified appraiser is required. An expert is needed to calculate the fair market value at the time of the donation, inclusive of accounting for any restrictions on trade relative to unrestricted ownership.

For Reliable, Authoritative Intellectual Property Valuations, Turn to BPM.

For charities, nonprofits and donors alike, having a qualified appraisal of this types of gift is essential. For the donor, failing to have a qualified appraisal could result in tax issues with the IRS. For the charity or nonprofit, it could result in costly and time-consuming re-statement of the financials.

This is where BPM can assist. Our collaborative professionals are experienced with all aspects of the donation process. Our team of valuation experts can calculate the fair market value on just about any gift, helping you secure adequate disclosure for your tax filings. To learn more about our valuation solutions for nonprofit organizations, contact Kemp Moyer, Directory in our Advisory practice and Head of our Valuations team, today.